Back

2026-06-25/Drew Hanover

Can Thermal Monitoring Lower Industrial Insurance Premiums?

Industrial insurance is rarely simple.

A broker may be excited about new fire prevention controls. A risk engineer may ask for more documentation. One carrier may recognize a system during renewal, while another may treat it as useful context but not apply a formal credit. The same technology can be viewed differently depending on the facility, industry, claims history, policy structure, and provider.

So the honest answer is:

Thermal monitoring can support insurance premium discussions, and some facilities do receive credits or reductions. But AVIAN cannot guarantee a discount. Your carrier decides.

That may sound less exciting than a guaranteed percentage. It is also the truth. And for industrial operators, the truth is still useful: a stronger fire prevention file can materially change the renewal conversation.

Why Insurance Providers Care About Fire Prevention Controls

Property insurers are in the business of pricing risk. For industrial facilities, fire risk is not abstract. A small heat source can become equipment damage, building damage, business interruption, cleanup, emergency response, environmental exposure, and a major claim.

That is why insurers and risk engineers look closely at fire protection systems, maintenance practices, electrical equipment, combustible materials, and documented response procedures.

Verisk's ISO Public Protection Classification program explains the broader principle clearly: insurers use fire-protection information to help establish appropriate fire insurance premiums, and better fire protection can create incentives through lower premiums. FM also publishes property loss prevention data sheets intended to help reduce property loss from fire, weather, and failure of electrical or mechanical equipment. Those are not AVIAN-specific sources, but they show the logic behind the underwriting conversation: documented prevention matters. ISO PPC program FM property loss prevention data sheets

For a facility, the key question becomes:

Can you show the provider that your operation is a better risk than it was last year?

Where Thermal Monitoring Fits

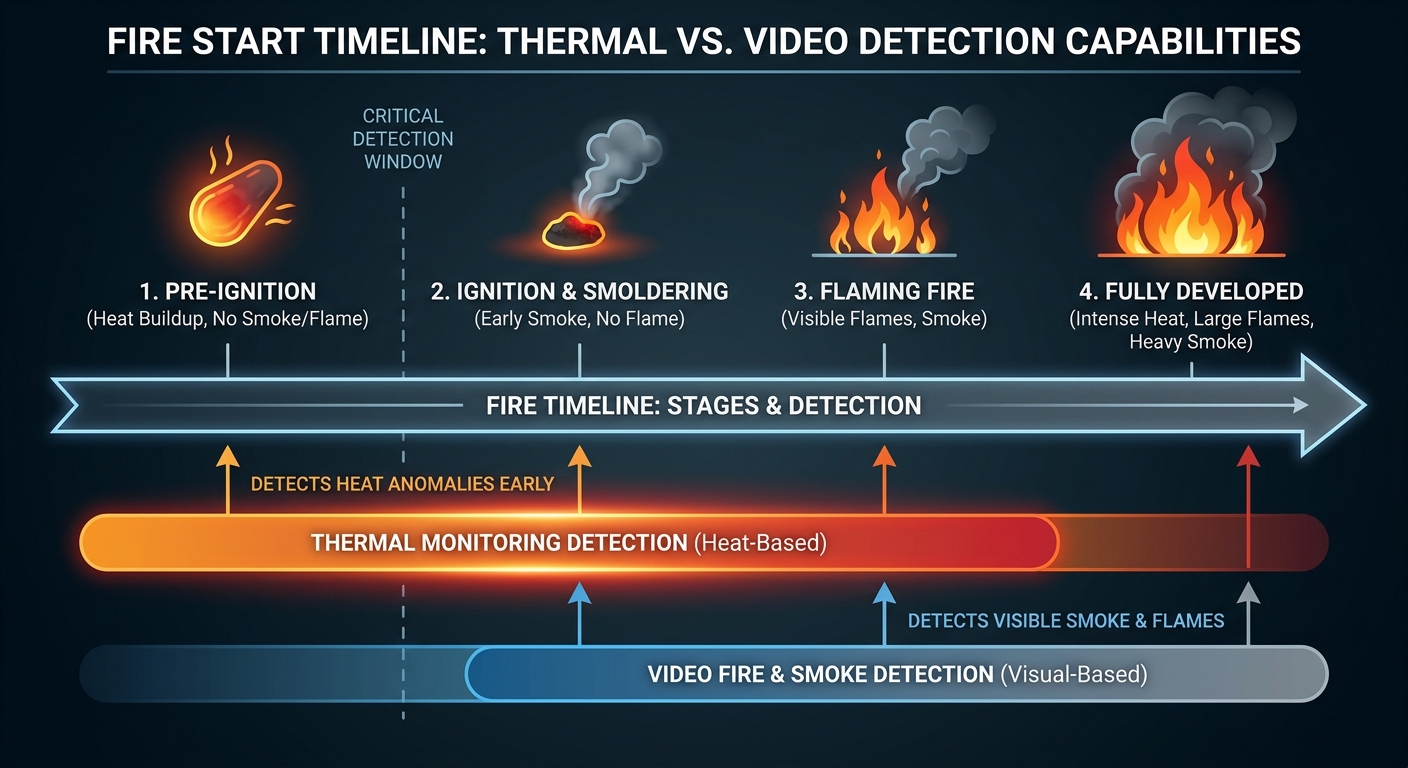

Many industrial losses begin as heat.

A bearing starts running hot. A belt rubs against a guard. A motor overheats under abnormal load. A loose electrical connection creates resistance. A battery or charger begins warming. A dust duct holds retained heat. A pile or load starts smoldering before anyone sees smoke.

Traditional fire detection is still essential. Smoke detectors, flame detectors, sprinklers, suppression systems, alarms, extinguishers, hot-work permits, and electrical maintenance all matter.

But those controls often enter later in the timeline. Thermal monitoring adds an earlier layer: it watches for abnormal heat before smoke, flame, suppression, shutdown, or a claim.

For insurance purposes, that matters because the facility can document more than intent. It can show:

- Which risk zones are monitored.

- What alerts were generated.

- Who received the alerts.

- What the team did in response.

- Whether corrective actions were closed.

- How the system supports written fire prevention and maintenance procedures.

That is a better renewal story than "we walk the plant and hope we catch problems in time."

What Kind of Discount Is Realistic?

Some AVIAN customers have seen insurance credits or premium reductions. Some have seen reductions around 10%. In one public customer story, Maple Rapids Lumber Mill coordinated with its carrier and received an insurance credit covering around 90% of the AVIAN system cost on an annualized basis.

That is a strong outcome. It is also not universal.

Insurance treatment depends on:

- The provider and underwriter.

- The broker's ability to present the case.

- The facility's industry and fire-loss exposure.

- Prior claims history.

- Current deductibles, exclusions, and coverage terms.

- Whether the system is installed in the highest-risk zones.

- Whether alert response is documented.

- Whether other fire protection systems are maintained.

- Whether the facility can show events, corrective actions, and procedures over time.

The safest way to frame the value is this:

A premium credit is possible. Risk documentation is useful regardless.

Even if a provider does not immediately apply a discount, a documented monitoring program can still support renewal discussions, deductible negotiations, coverage conversations, internal risk reviews, and post-event analysis.

What to Send Your Broker or Carrier

If you are installing thermal monitoring partly for the insurance benefit, do not wait until renewal week to mention it.

Build a simple insurance packet around the system.

Include:

- System overview. Explain what AVIAN monitors and what problem it is intended to solve.

- Coverage map. Show monitored zones, assets, cameras, blind spots, and priority areas.

- Alert workflow. Document who receives alerts, how escalation works, and what happens after hours.

- Response procedure. Connect alerts to inspection, shutdown, cleaning, isolation, maintenance, or emergency response.

- Event examples. Include thermal images, timestamps, alert records, and outcomes from real events.

- Corrective actions. Show how maintenance or operations closed the loop after each event.

- Integration notes. Identify any PLC, shutdown, suppression, or reporting integrations.

- Maintenance records. Show that the system itself is maintained and reviewed.

This is the difference between saying "we bought thermal cameras" and showing "we have an active fire-risk monitoring program."

Questions to Ask Your Insurance Provider

The best insurance conversations are specific. Ask questions that force the provider to tell you what matters.

Useful questions include:

- Do you recognize continuous thermal monitoring as a fire-risk control?

- What documentation would help during renewal?

- Are premium credits, deductible changes, or improved terms possible if monitoring is installed?

- Which zones or assets would your risk engineer want monitored first?

- Do you require evidence of alert response, corrective actions, or integration with site procedures?

- Would a quarterly thermal event summary be useful?

- Are there specific standards, inspection intervals, or documentation formats you prefer?

The goal is not to pressure the provider into a generic discount. The goal is to learn what proof they need.

Where AVIAN Creates the Strongest Insurance Story

The insurance case is strongest where fire risk, downtime risk, and monitoring gaps overlap.

That often includes:

- Sawmills, planer mills, and wood products facilities.

- Recycling and waste operations.

- Biomass, pellet, and bioenergy plants.

- Grain handling and feed mills.

- Ports, terminals, and bulk material handling sites.

- Food and beverage manufacturing.

- Battery charging, fleet depots, and energy storage areas.

- Data center infrastructure and electrical rooms.

These facilities often have combustible material, hard-to-monitor equipment, night or weekend exposure, and high business-interruption consequences.

Thermal monitoring is not the only control an insurer cares about. But it can make a facility's fire prevention program more visible, more documented, and easier to evaluate.

The Bottom Line

Do not buy thermal monitoring only because someone promised an insurance discount.

Buy it because abnormal heat is one of the earliest signals of fire risk and equipment failure. Buy it because the same system can help prevent downtime, protect assets, route alerts, and document response. Then bring that evidence to your broker and carrier.

Some facilities may receive meaningful insurance credits. Others may use the same documentation to support renewal, protect coverage, or answer risk-engineering questions.

Either way, the strongest position is the same:

Show the provider what you monitor, how you respond, and what you have prevented.

For a deeper look at the insurance-facing workflow, see thermal monitoring for insurance risk reviews. If you want to map coverage for your own facility, contact AVIAN and we can help build a risk-review packet around your highest-priority zones.

Drew Hanover

CTO & Co-Founder

Get new AVIAN insights in your inbox

We'll send practical notes on industrial fire prevention, thermal monitoring, and customer learnings. No noise.